Unless something changes drastically I will end 2015 up 18% TR (Total Return) this is pretty much straight in line with my usual level of return – circa 20% per year. It is way below my target of 30-40% per year.

FTSE 100 TR – circa flat

FTSE 250 TR +12%

AIM AS CR + 4%

FTSE Fledgling (CR) +13%

It is not enough.

Due to the size of my capital base I could reasonably easily earn this by simply working full time or in a more demanding job, leaving my money in the hands of the professionals.

The money I gained this year is simply not enough for the effort I am putting in… Having said this working doesn’t compound as well as investment – I may earn more but it wont grow exponentially as investment earnings (hopefully) will. I am only 36 so have many years of compounding ahead of me.

So I will continue, and next year is another opportunity.

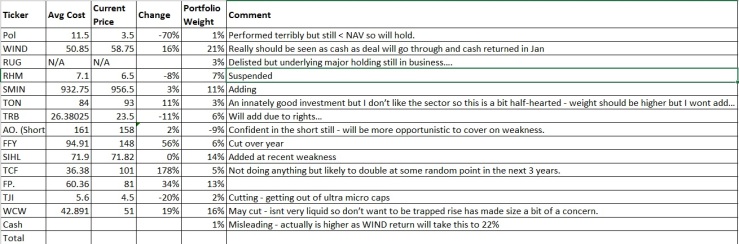

Portfolio looks like this:

There is a bit of uncertainty as to the value of RUG – Renn universal growth – see post here. And RHM – posts here and here .

Anchor Free – Renns major holding appears to be difficult to sell – but it is still trading well and I am happy to wait – it certainly isnt worth 0 and I dont know if its worth what I paid for it. I therefore value this at cost less capital returns – it isnt terribly important.

RHM will have much more impact – at a 7% portfolio weight. In retrospect this is far too much given the illiquitity and size of the company. Still RHM’s 40% stake in PUC Founder – which is much more liquid is worth about £8m – double RHM’s market cap. RHM also has about £4m in cash – to be reinvested in PUC founder. Putting it together you get to double the current price at least. I doubt and sincerely hope I wont walk away from this with less than I went in with but once a delisting happens I am at the edge of my knowledge.

If I assume both RHM and RENN are worth 0 I get a return of 6% this year, I dont however think that is the case.

On this years posts.

Smiths industries – too early to say.

Tribal – down slightly -11% – can soon turn round am highly unconcerned.

AO world – I have been right on this but haven’t been able to make much money on it – shorting is a skill I am yet to master – I will keep on at it. I am convinced this will fall further. I think I need to be quicker to cover on sharp falls. Its worth persevering as I will get better with time and shorting is a valuable skill I want to develop. I will actively look for more shorts in 2016.

Walker Cripps – up 23% including dividend – I believe this is slowly playing out. I may cut it a touch as the portfolio weight is a tad heavy.

Tinci – always nice to be 100% right

Invista European Real Estate Prefs – got out at a 32% loss – in retrospect a good move as it went to 0. I often think part of the reason for my success is how I manage the losers, not the winners…

Tejoori – getting out of ultra-microcaps, will liquidate eventually.

SCS – got in at too high a price, small profit…

Titon – still got a solid investment case but spread of 7.5% is far too steep. Not sure if I want to hold as I am getting out of microcaps – then again, investment case is intact and I have reduced.

ACHL – too early to say – stock down further at time of posting.

Wind – has worked out completely – an easy 20% – on about 20% of my capital. For the more slam dunk trades like this I am thinking of using my spreadbet co’s guaranteed stops to put a lot more size on to boost returns….Not sure if I will be able to do this – one for 2015….

Other things I have done over the year – liquidated my man group holding at an average of 169- this was a very big position so contributed a lot to realised returns – realised profits alone were 10% of my portfolio.

Lightened FFY a lot – it is up circa 50% and I wanted to derisk my portfolio.

Next year I am going to try more shorts and I will look overseas more rather than going down the cap scale / reducing quality. My method (such as it is) works best where markets are in bear markets – so I will go to look for them.

I strongly suspect my returns will be largely driven by the performance of Tribal and Smiths Industries. Symphony may well also rise a lot in price. With a NAV of $1.16 (much of it listed) and a price of $0.71 good things can only happen this discount is just too wide added following recent falls.