I bought Lenenergo Prefs last week at an average of 168. This is a 3% weight, I am also re-entering EOS Russia – a fund holding Russian grid companies, also at a 3% weight.

Continue reading “Lenenergo Prefs – 10-15% yield & EOS Russia – Adventures in Russian Grids”H1 2021 Review / Portfolio +13.8%

Thought I would do a review of where the portfolio stands.

As at end June I am +13.8% for the year, roughly matching the FTSE AS at c12%. it has been far more volatile than is usual, pre-fed comments on tightening sooner than the market expected, I was up closer to 20%. The volatility is driven by the large exposure to natural resource co’s and volatility resulting from their underlying commodity feeding through to share prices, which are, in turn, even more volatile.

Continue reading “H1 2021 Review / Portfolio +13.8%”Exiting Russian / Ukranian positions, possibility of invasion not priced in

I’ve decided to sell up on most of my Russian / Ukranian stocks.

HYDR, FXPO, SIBN, RSTI, GLTR.

I am holding on to FEES (Russian Electricity grid Yield 8.5%+, P/E <4 and P/B<0.3 (I can take the pain on this), and GAZP as 50% dividend payout news announced today implies *potentially* a very high yield.

I am increasingly concerned there will be an invasion/incursion in Ukraine. This build-up seems long/ sustained for a ‘training exercise’. If they go home without doing anything Putin will look weak.

I also note last year their western district held intensive training exercises as well.

He will be especially wary of talk of Ukraine joining Nato, in Russian terms this is equivalent to Canada joining the Warsaw pact – something that can’t be allowed to happen!

Continue reading “Exiting Russian / Ukranian positions, possibility of invasion not priced in”My first podcast

Recently did a podcast with Brandon Beylow (@marketplunger) on the value hive podcast.

You can hear it via Apple podcasts here

or google podcasts here

or spotify here.

Enjoy, views appreciated, subscribe to his podcasts, he has lots of great, left-field guests.

Tharisa – ridiculously cheap, High Rhodium Price means a likely PE well under 4

In recent months I have been investing more in natural resource co’s. Focussing on Uranium (URNM, KAP, YCA (now sold for more URNM). I bought copper via COPM and CAML as well as gold/ silver via metals holdings and AAZ (free mines following the Azerbaijan/Armenia war) as well as TSG and a few others….

Now my portfolio is c48% natural resources with 10% gold/ silver metal. I bought Tharisa a few weeks ago to add to this replacing my holding in JLP, as I think this is better…

There has been disruption in production due to COVID , but the main reason I am in is (in the main) due to developed world money printing. I believe this will be inflationary so resources that can’t be printed are a good place to be. Think about it like this, if the stock of money increases (say) 25% then any fixed quantity in the economy should also increase by at least this. Of course, reality is not that simple as demand/ production increases / decreases. I believe this printing is not like that which occurred around 2010 as that was to recapitalise the banks so just sat on their balance sheets so wasn’t inflationary whereas this will get out into the ‘real’ economy.

Continue reading “Tharisa – ridiculously cheap, High Rhodium Price means a likely PE well under 4”Blast from the Past – Renn Universal Growth – Finally Money Returned

Very brief post on this.

Back in December 2014 some of you may have invested in Renn Universal Growth.

It was a liquidating investment trust worth £2.95 with an offer price of £2.24 and £1.68 in liquid assets. Post on it is here.

Continue reading “Blast from the Past – Renn Universal Growth – Finally Money Returned”Steppe Cement $STCM – Kazakh Cement Company

I put a position on in this a couple of weeks ago @33p, its risen strongly since but is still a buy at 40p. Its a neat little company which hasn’t been widely covered (as far as I am aware). It has a healthy 6-8% yield. Pretty much all earnings are paid as a dividend. Its trading just above book value. My current position is a 3.5% portfolio weight, which feels a touch light. I am still adjusting to growth in the size of my portfolio and don’t want to be too heavy in illiquid stock, I may well add in time as this plays out.

Continue reading “Steppe Cement $STCM – Kazakh Cement Company”2020 Full Year performance +49%

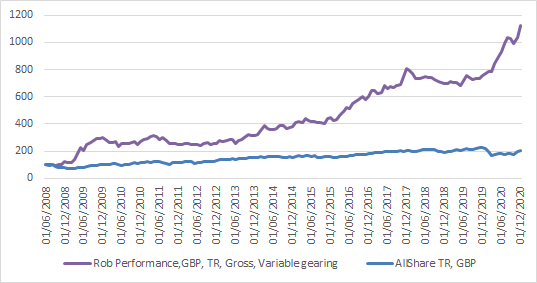

As it is getting towards the end of the year I thought I would do my traditional performance piece.

I am at roughly +49% ytd. A reasonably good performance – though as ever there was lots that could have been done different / better. That is with a cash/gold/silver position of c30% for most of the year, though at times I have been slightly levered, I am also helped by keeping cash out of sterling.

The long term performance chart is below:

Q3 2020 Review +12%, + 39% YTD

A very quiet quarter for me. I have made very few changes. This is being written a few days before the end of September so figures may differ slightly, but baring an unexpected disaster / triumph this is roughly where I will be…

- Got rid of EOS Russia – no real reason – it just hadn’t performed well and a realized loss is good to manage my CGT position. I may well re-enter.

- Sold some Beximco on a ridiculous spike buying some of it back lower down – I will refill my position again lower down.

- Sold a bit of CMC Markets – as my position was a bit big and wanted to buy other things.

- Sold half my SERE on a dip – this was an unwise panicking out on something of a headfake. Could be summer ‘silly season’ low volume move. I am noticing more stocks than usual falling with no reason.

- Sold half GPSS to take some profit.

- Most impactful change was buying 4D Pharma in the placement. This has done brilliantly for me – more later.

My portfolio is below:

Continue reading “Q3 2020 Review +12%, + 39% YTD”Q2 2020 +24% (+33% ytd), but still nervous

Quick overview of performance – and holdings which I know is something you all enjoy.

At the end quarter I am c+24% ytd. This is vs a FTSE AS of -17%. and AIM AS of -8%. I have had a very good July and am currently up c33%.

This is good but I often think of a (mis) quote when I am doing well:

“Those whom the gods wish to destroy they first make invincible”

Continue reading “Q2 2020 +24% (+33% ytd), but still nervous”