As it is getting towards the end of the year I thought I would do my traditional performance piece.

I am at roughly +49% ytd. A reasonably good performance – though as ever there was lots that could have been done different / better. That is with a cash/gold/silver position of c30% for most of the year, though at times I have been slightly levered, I am also helped by keeping cash out of sterling.

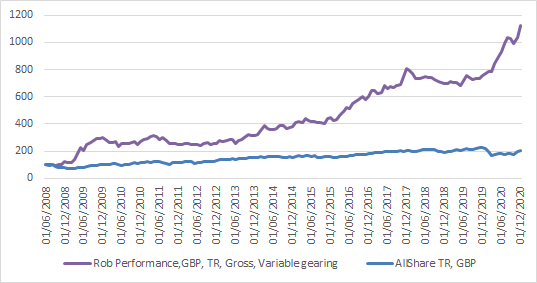

The long term performance chart is below:

I am particularly disappointed I didnt buy more natural resource co’s back in April. I was able to do my usual, investment trusts at a discount play, that, as ever, worked nicely. It’s easy to look back with 20:20 hindsight and say you should have invested more then. To me, it wasn’t obvious that governments would throw a veritable wall of money at business. The long run consequences of this are very much to be determined. It’s very difficult for me to operate in natural resources as its far from my usual area. I still think that these will likely be the investment of the 2020s so I intend to be well positioned with a 30-40% weight ASAP. Unfortunately, progress has been slow. I think much of the problem is so many smaller resource co’s trade below book I don’t believe book, maybe I should be more trusting / less cynical.

At the beginning of last year I was determined to quit my job / move abroad and invest full time. I still haven’t done it, corona has made it more challenging… I have cut hours slightly to 3 days a week. But it really makes little sense for me to continue with a job outside the safety net aspect and the fact that, if I quit my (already extremely poor) employability rapidly diminishes… On a down month its comforting to have a steady salary.

I have made c8 years (net) salary or 9 years worth of spending this year (and I have spent a lot more than usual this year). At the moment, the portfolio is 25 year’s worth of this year’s spending or c35 a more normal year. That doesn’t include property income / the ability to liquidate my properties. It’s a definite goal for 2021. I will be very disappointed if I still have a job at the end of 2021. Having a job has almost certainly cost me a multiple of the income earnt from doing it.

On a more positive note, quite a bit of this year’s strong return has been driven by me being better at cutting straggler’s. Not so much stocks that have not performed well but ones which went nowhere. Key examples would be AJOT – deep value Japanese shares. Its right up my street but the share price is basically flat and I believe the pandemic / lockdowns is a very good argument against reform and in favour of the lazy balance sheets many Japanese corporates love. I actually think that companies with heavy balance sheets should be more valued by investor’s generally, they should appreciate the stability they give, but that’s a million miles away from current psychology. Having said that, in a world where government’s readily turn on the money printing presses / make funding easily available there isn’t much of a need for fortress balance sheets….

Other stocks that didn’t move include DCI – Dolphin Capital – surely the longest liquidation in history, dont management remember they are charging shareholders fees !$~!. I will give it one more year. ALF – had been a strong performer, returning a multiple of my original investment but hasn’t done much the last year. In two minds whether to sell it.

My Russian / Eastern European holdings have done reasonably well. The performance has been hit by a c20% fall in the rouble vs GBP so I am up in Roubles but not so much in GBP, large dividends help too, and are part of why stocks don’t appreciate in capital terms. I still believe GLTR – Global Trans is a great deal. It has a forecast yield of 17%. It is forecast to pay a 16% yield in 2020 (don’t forget Russia’s 15% withholding tax). It now has a listing on MOEX for those of you who don’t like GDR’s. My positions in RSTI, RSTIP and GLTR are far too small and need to be substantially increased. I also bought back into HYDR, which I should never have sold, clean energy, 0.55 P/B, c8% forward yield, 6 PE, should be far higher, particularly with ESG investing becoming more of a trend.

On to the portfolio:

So in terms of big picture weights – I am happy but as I mentioned I have too little non-uranium natural resources. As an FYI, there is (to me) a pretty good uranium bull case out there. FYI interesting thread on YCA is here (interesting though I don’t think its going to happen).

Some good resources on the past boom is here. (seriously you have to read it, even if you aren’t interested in Uranium, it is very insightful)

Rough outline to the uranium bull case is here.

Cash/Gold/Silver is a 12.58% weight (I haven’t sold any but other things have gone up). ASTO (Still my largest holding) has had a tender offer for half its shares so I should get another 5% of the portfolio back on around the 11th of January.

I intend to be more fully invested in future, avoiding the large cash positions I have held in previous years. At times this year I was 30%+ cash! I may well go levered if the opportunities are there.

Number of holdings is a perenial problem. I can’t run as concentrated as I used to. I am not in as many simple / low risk liquidation plays. There is much more risk in Russia / natural resources so I am wise to spread my bets. I am far less confident than I was when I was going from liquidating investment trust to investment trust, sadly that game is done for the foreseeable… The risks / rewards are far higher in Russia / resources and my other holdings (with a few exceptions). The downside is I look into things with less depth and don’t monitor as well – which is true. In the short term I am not a great picker of what will go up – for example, I consistently like FEES / GLTR, which inevitably go nowhere quarter after quarter. Though with a double digit yield, most years I can wait for the rest of the world to wake up. Can’t delude myself though – hard to get good performance on the portfolio as a whole if I hold stuff like that. The rest of the portfolio really needs to move fast to keep up.

I have some concern as to the general market environment. Leading stocks such as TSLA are stupidly valued. Amazon is on a P/E of 92 (I understand the flywheel argument that it isn’t overvalued, I have my doubts). AAPL is on a PE of 40, it’s not far off doubling since the beginning of the year, profits barely up 10% on 2017. Somewhat depressing to note that just buying the leading FANG stocks substantially outperforms all the effort I have put in over the last 5 years. Still I won’t buy, I realise I need to invest in accordance with my personality (cheap) and I am far from early on this one….. I am far less convinced these businesses have the ‘moats’ people think they do. I know many people who are deleting Facebook. I remember how easily and quickly Blackberry/Nokia were replaced by Apple / Android.

The risk is that, even though I am not in these stocks if they take a dive then my stuff will be taken down with it – something I am keen to avoid. This is a risk that is potentially, and I think probably, years away, however I will bear it in mind as best I can when managing my exposures. I really want to hedge it by buying TESLA puts, but having looked into the competition I think early 2021 is not the time. Better to wait till mid 2021 / 2022. More generally implied volatility has fallen substantially and it might soon be cheap to buy puts again.

Outlook for 2021 is hard to call. Lots of money has been printed and will be printed until the pandemic is over, feeding through to asset prices. Will taxes rise? I tend to think no, we will print until money is debased, as has happened multiple times in history. Many asset prices are too high now, rates cannot ever rise without an extraordinarily painful collapse in prices far easier to print/ manipulate statistics / feign shock at inflation. Unlikely to happen in 2021, I would assume it would be many more years for it to feed through from the financial world to the real world.

More concerned at the prospect of a virus resurgence / evolution so vaccines don’t work. I’m surprised more people are not thinking about this. The (western) population is likely to be vaccinated over 3-6 months – quite a long time really… If you think about this from an evolutionary perspective, selective pressure is put on the virus. It may then evolve into a form which can infect people who have been vaccinated. Worse, the ‘new and improved’ UK strain replicates more (which is why it is more infectious) so (in my view) is more likely to mutate if not stopped. This is well out of my lane, I am by no means a scientist but can use logic and reason well. A counter to this is that multiple vaccines work in different ways so may prevent any prospective mutation spreading.

Goal for 2021 is 30%+ returns. To get there I either need to cut slower moving stocks or increase holdings, even to the point I am slightly levered, in faster moving stocks / stocks with catalysts. Right now I plan to increase holdings. I doubt many of my slower moving stocks will fall too much in the event there is a pullback. Many of my stocks tend to be asset based – such as ALF, DCI, WCW (hopefully), ASTO. If I go more heavily into resources then I will need to be sharper in hedging / exiting ahead of pull-backs.

I am also looking to put together a social-trading portfolio on etoro. For those of you who don’t know etoro is a platform where you can copy other traders. So you could copy my portfolio (and I get a small fee). The issue is I can’t create a portfolio replicating my actual portfolio as many of my favourite stocks aren’t and never will be available (they keep it liquid for obvious reasons). So I need to tweak it, likely won’t get this started till mid-year at best.

In terms of blogging I am planning to *hopefully* only do a run through of holdings at the half year and go back to more posting on ideas, but this very much depends on what good stuff I can come up with. Issue this year has been there has been a lot to do with very little time so I have been putting tweets out here @deepvalueinv.

Wow great results Rob. Congratulations! Sounds like you need to quit your day job yesterday 🙂

Thanks for the congratulations. Yeah I need to get it done.

Good luck on leaving the workforce! that sounds amazing

Thanks Dan

Any reason why you bought North Shore Uranium Fund as opposed to just sticking to individual Uranium stocks?.

I myself hold Canada’s Uranium Participation (U).I was holding Centrus (LEU) on NYSE but sold it stupidly just before it spiked up 150%

I dont generally invest in US / Canada listed stocks – I stick to the UK/Europe/Russia. Different game / rules over there that I dont know and am not good at so I will go passive. Am not a mining specialist so not entirely comfortable.

Superb year, congratulations, I am rather jealous.

I’m familiar with Just Group, I wonder what your reason for holding them is, doesn’t seem to fit your thematic approach?

Thanks, I wouldn’t be jealous – I look at people earning returns in the 100s of percent and wish I was them….

I disagree I have a thematic approach – I tend to think I am more eclectic generally – I can see why it might look that way.

Just is very low price to book, in a decent/growth sector.

Hi RJ, congratulations on the performance! Your personal note of wanting to leave the workforce to focus fulltime on investing has got me wondering, how do you currently balance the two – i.e. how much time do you currently spend on your personal portfolio outside of (what I presume to be) a full time job? Anyway, very envious of your prospect of going at this full-time, best of luck!

Thanks, I don’t work full time – until October it was 4 days a week, now 3. Thanks for the comment / good wishes.

Great performance. If you give up the job, you will have more time. It is possible that you become too active (more frequent buying/selling etc), which doesn’t necessarily increase the performance (?) Also I wonder if a deeper analysis has really more benefits. It is amazing that you achieve the performance also with big stocks/companies (personally I buy mainly nano stocks.There is hardly any competition from institutional investors for very tiny stocks).

to give an example that (over) activity can be very bad. I bought some Nautilus stocks (NLS) at about usd 1.3 in 2019. I sold them for about 3.3 in 2020. I thought this is a great return.

But Nautilus trades now for over 20!

[…] to my usual review of the year (last years here). We are slightly shy of the full year end but I recon I am up about 20.5%. This is in my usual […]