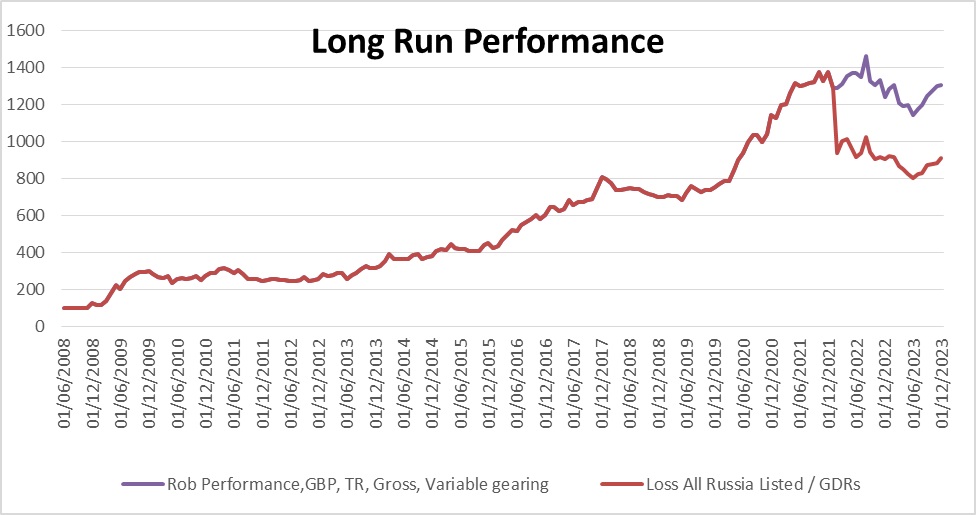

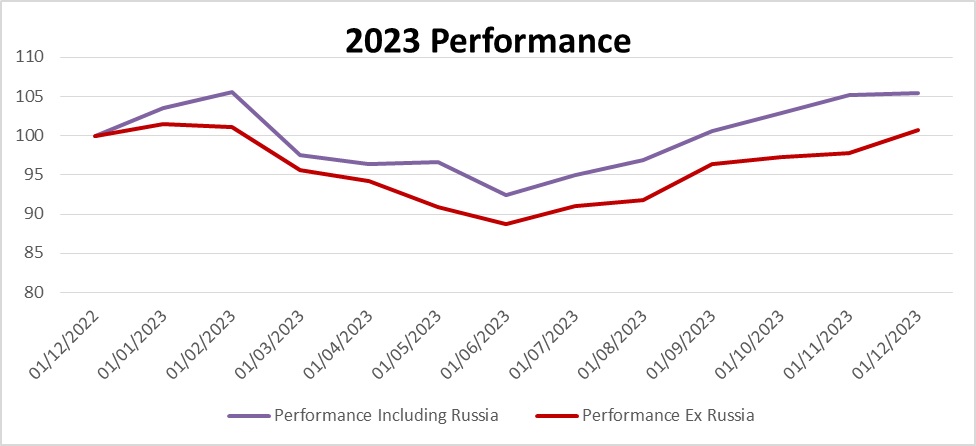

Usual end of year review here. It hasn’t gone well, overall +0.8 (excluding Russian frozen stocks) or +5.4% including Russian frozen stocks. If Russia goes back to normal will be up far more as there are a lot of dividends waiting to be collected, not included in the below.

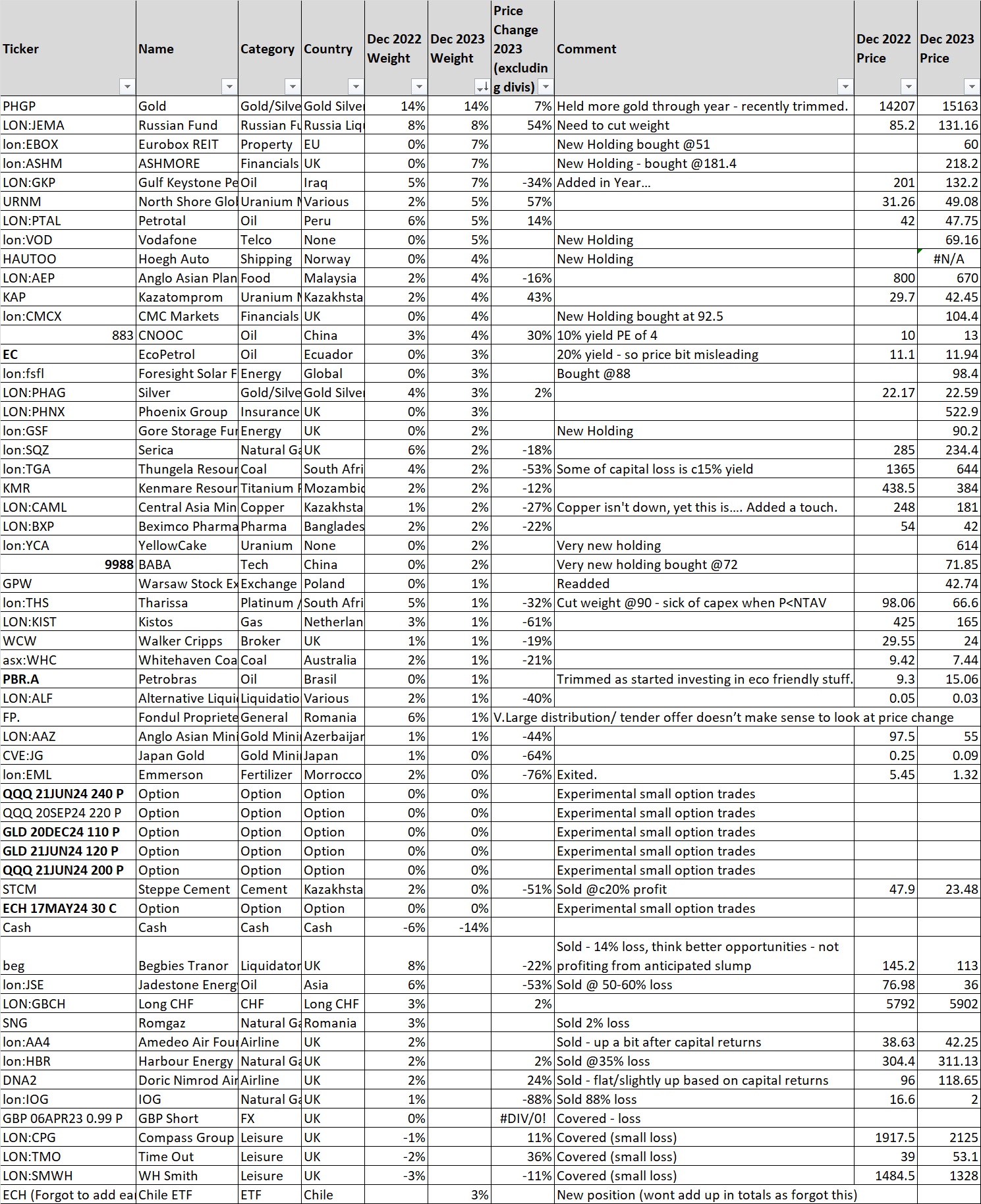

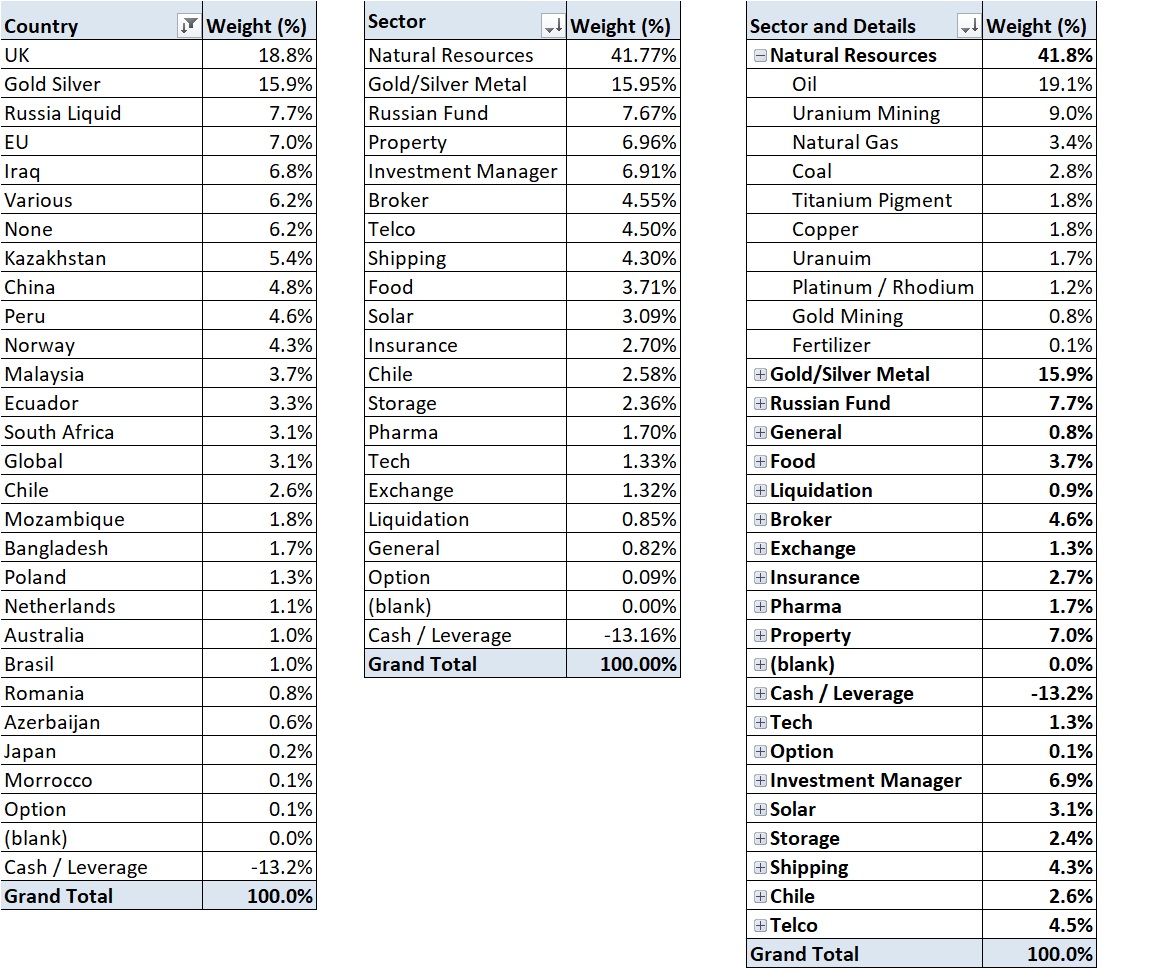

Linking back to last year I was pretty much wrong about everything. I was heavily into natural resource stocks (c57% weight vs 41% now), not the best sector in 2023. Some of the fall in weight is due to me mildly cutting weights as stocks didn’t go my way / though quite a bit is due to price falls. I had moments of good judgement – saw the possibility for political change in Russia – which very nearly came about with the Prigozhin mutiny, got into financials late in the year. Broadly things haven’t worked. There is a mild positive element to this – if I can be pretty wrong on almost everything and still not lose *much* money it’s not too bad – but it’s far from ideal given time I put in / potential returns. It’s also positive I havent gone off the rails after the large Russian loss last year – its easy to chase / raise exposure, which is something I don’t think I have done. There is an argument around stops – which I don’t use – going to be a little more careful with stocks bought at highs – particularly Hoegh Autos.

Weights are below:

Figures are as at 23rd Dec – so a little approximate – but a generally accurate flavour of where I am. (some very illiquid stocks like ALF prices are incorrect…

Not inclined to change sector weights too much, less precious about stocks. I have also been quite badly hit by production problems, AAZ had tailing dam issues, PTAL – issues with the natives, JSE – production problems. Not sure if this is just dumb luck or some of these problems were in the price – I certainly knew PTAL had problems with ‘community relations’. JSE’s problems with their FPSO (floating production ship) could have been forseen if I had researched better – important to look into age of vessels, didn’t know/think to do it at the time however. These few hundred million market cap stocks are much more vulnerable than I thought- cash piles can evaporate very quickly if they hit issues.

Moves in some of my larger weight resource co’s that I continue to hold have been unfortunate – CAML -27%, KIST -61%, TGA -53% and THS -32%. Whilst gas and coal are down substantially copper is about trading at the price it was at the start of 2023, Tharisa’s basket isnt down that much. CAML is trading at a PE of 8, 9% yield, THS PE of 3.5, 1/4 book, though marred by a management who insist on growth capex whilst trading sub book. They may get lucky if prices rise but it’s luck, not judgement. TGA, also very, very cheap 7% yield, low single digit PE, again, irritatingly, investing rather than returning capital. These large falls are not wise from a capital preservation perspective, one needs a 100% rise to counter a 50% fall. But if we do get a pick up in the economy / resource prices these could easily get back where they were. There may also be an argument these can just rerate with the market, though at present they just seem to be disliked. PTAL seems to be doing well with decent prospects and a 10%+ yield, with buybacks – all depends on the oil price. Downside to all this is being commodity producers they only have so much control over their fate – why many investors dislike them.

A stock which has had production issues is GKP – Gulf Keystone Petroleum it’s issues concern the legitimacy of it’s production contract / pipeline access. It’s the only one I have added to rather than reduced over the year – averaging down. The whole Kurdish oil industry has a question mark (depending on who you listen to) regarding the legitimacy of it’s contracts. But, I can’t think of an example where a whole industry was seized / nationalised / expropriated. Everyone – Kurdish govt / Iraqi govt and oil companies have said that contracts will be respected / discussions are ongoing. It is far from risk free – I suspect biggest risk is that one company is punished / seized to encourage a deal to be made by the others. Huge upside on this – it’s a very large field with very low extraction cost – even though the oil isnt the best quality, if made legitimate depending on the exact deal. They are more than covering their costs so in my view worth a look if you have risk tolerance for a substantial loss. If this works it is a 3x-5x or more, but it is one where the outcome is largely outside management’s control – for reasons other than commodity prices.

One of my best performing investments is JEMA – formerly JP Morgan Russia. It is an odd one – trading at 48p ‘official’ NAV with a share price of c £1.30 and a MOEX NAV at about £5-£6. JPM have marked all the Russian holdings to about 0. I am up about 55% and have trimmed the position – selling about a third already. There is growing talk of seizing Russian assets to pay for the next round of Ukraine funding. Not entirely sure what to do on it – upside is still huge but I already have 30% of the portfolio value in Russian, sanctioned stocks. I dont really need an extra weighting to turbo charged Russian exposure with the same risks – going to have to cut this to manage risk but somewhat reluctant to, given the upside… I believe a lot of the frozen Russian assets are held by Clearstream in Belgium , but unsure to what degree Belgium really makes the decisons on that one. Russia appears to have ‘won’ at least to some degree militarily – they are making gradual progress, however they are keen to have ‘peace’ / cease fire talks. I suspect this is because their wins are not sustainable, human losses/ financial cost is too heavy to be sustained. Ukraine lacks the manpower and potentially arms for an ongoing attritional fight but Russia lacks the motivation. My view is Russia cracks first and we see more mutinies in 2024.

Uranium trade has gone well – KAP/URNM up 43/53%. Have switched a little bit of money out of URNM into YCA – maybe the metal will continue to outperform the miners for quite a while. I am somewhat skeptical of YCA / SPUT buying Uranium to tighten the market – as an industrial commodity – it only really has value if it’s used – so implied price of spot / spot -% means one day it will be used, and if it will be used then tightening of the market probably shouldn’t happen. Not how people are looking at it at the moment though.

Financials have done well – despite me adding Nov/Oct so they haven’t had too much time to contribute. October prices for lots of investment trusts / asset managers etc. (mostly UK based) looked very depressed, 10% yields 40% etc discount to book values. Startling how quickly things have bounced. Not entirely sure best way to handle these longer term, they could be a nice solid income play, bought at high yields or if I find something better then time to sell . I wrote about these recently in this post. I am a bit concerned about them as a longer term hold – the upside is very much limited, though high probability. I prefer to be in the ‘real’ inflation linked economy, hard assets rather than the financial economy.

A financial I bought after that post is PHNX – Phoenix Group – this is a large closed life insurance manager it’s trading at a decent 9% yield. The dividend is £500m for a company which is generating £1.3-1.4bn pa in cash and which has £3.9bn solvency 2 surpulus – it should be sustainable. As ever with hyper large-cap insurers as an amateur you are never quite sure what the regulator will come up with which will ruin your day. You are also betting against the new weight loss drugs increasing lifespan – though of late expectancy has been falling unexpectedly. Not one I will hold for too long – I am thinking about a year or two, but I think it is under-priced. Seeking alpha write up here (not by me).

Sold out of AA4 and DNA2 – decent profits on both (+100% on some tranches, held since 2020) but I think there are better places for funds now. I may be missing out on a bit of upside if the A380 finds more of a market – perhaps if another airline starts using it, though I doubt it is logistically simple. There are now better opportunities out there, though AA4 may have more upside but at higher risk.

Fondul Proprietea is now a tiny weight – after tender offers / returns of capital. Its a little sad to be saying goodbye. I came up with this idea back in 2012 and have benefited from a closing of a 50% discount and growth in underlying investments – it’s really the ideal investment. It has had a 962% rise since inception (2011) and I have owned it since 2012 – though on occasion have had to drop it due to broker issues. Time to sell this – as there isn’t too much upside left now. Really struggling to find things with this level of quality / cheapness / ongoing compounding opportunity.

Having said this, one which may fit the bill is Beximco (BXP) this is a Bangladeshi Pharma, trading at a PE of 5, doubled revenue since 2018 (in BDT, but even in USD it has grown impressively) and it has substantially increased earnings (my 2019 write up here). It is currently trading at half where it is in Bangladesh but there is no arbitrage opportunity. Frustratingly, I had to cut my weight as my broker wouldn’t allow it in a tax efficient ISA account, this didn’t hurt me as the price fell. My broker has changed their mind so now I can put it back and raise the weight. Brokers here seem to rely on large screening firms and drop / add firms to the list of what is eligible – not depending on the rules but how they feel at the time.

Walker Cripps is very much the worst kind of value investment – the one where nothing happens. Walker Cripps is cheap on an AUM basis but hasn’t moved since I bought it in 2015. Possibly I have given this too long, then again there is consolidation in the sector and this would be perfect for it… The FOMO of knowing the day I sell it an offer will be made at 3x the current price keeps me holding, my not insubstantial patience is running out.

I still have some leverage – but that’s cheap mortgage / unsecured debt at 3/4% rates. Its a relatively small amount vs portfolio / portfolio + property assets – about 20%/11%. In effect, as in prior years leverage is being used to buy gold / held on deposit at a higher rate…

In terms of life – no change, still living in the UK, rather unhappily employed (low/mid level data analyst) three days a week, doing investments / little bit of property the rest of the time. Really looking forward to life starting properly when I am no longer employed / ideally leaving the country. Was somewhat distracted by a pointless court case during the first half of the year and didn’t see much opportunity so didn’t do much. Second half has been better, particularly after October. I still think a big move in many of the resource co’s I hold is likely, so really dont want to move before that happens – as a country move will entail pulling quite a bit out of stocks. PE’s of under 5 are not likely in my view to be sustained, though there is a risk a sustained recession / depression shrinks earnings and share prices further… I’d like to get more copper / tin / silver exposure but haven’t yet found any stocks I like, and ETF’s are not without their problems…

Think this year has suffered from me mostly being in decent stocks in terms of yield / valuation but not stocks the market cares about / likes which is why they are cheap. I could go more mainstream but I’d rather stay where I am and wait for the market come to me rather than chase… Not wedded to particular stocks but the weighting to the resource sector needs to remain – they have been under invested in they are cheap and unfashionable – very much think they will have their day in the sun. Plan to switch back from some of the finances to resources once the financials get back to closer to what I anticipate is their fair value.

Stocks I plan to look at next are tobacco – BATS/IMB probably – if I can get comfortable with legal risks / debt levels, they are yielding well and are not highly valued. When I can buy mainstream stocks at single digit PE/ EV/EBITDA there is no need to go too far into exotic territory. Not the most popular – they do kill their customers after all, but vapes, cannabis etc may provide an opportunity to actually buy growth at a low price – particularly if regulation cuts out dodgy Chinese imports. Still want to rebuy Royal Mail at the right price. Longer term I want more Latin American / Asian listed stocks. China looks cheap but I am very wary of avoiding a repeat of the Russian situation.

Best of luck for 2024 – as ever comments/views appreciated.

good luck for 2024. you didn’t post much at all and i wondered what happend.

For me nice outcomes on Lehman ECAPs, SNS bank claims, Polymetal stock, trading Ru ADRs and Bonds was the highlight.

Wasnt active in early 2023 really, Sad I missed Poly – I was watching but I have too much Russian stuff so keeping away. What are Ru ADR’s going for nowadays ? How do you trade them ? Any views on likelihood of asset seizures increasing?

On the RU ADRs

As a firm we are buying mostly directly from institutions and selling to others. mostly traded at around 50% of MOEX. Some real outliers of course with anything SDN much lower or almost impossible whilst a few above 55%.

I think the Re-Domicile of Yandex and Tinkoff will lead to the trading in their ADRs becoming much more infrequent and more difficult. Generally the re-domiciling willl i think open the door to Western investors being much more likley to be wiped out, through technical changes or being barred from new share purchases.

We are seeing a mirror image of that in the way that the EU/Netherlands is “wiping out” the Sberbank/VTB shareholding in Agrokor, by way of a sale of the operating Co’s at a rather reduced price and the two russians being barred from voting or participating. https://www.fortenovagroup.nl/Press ( top story )

Poly has been very nice, bought UK stock, not Kaz registered.

To trade them its not so simple, but with a account at a Cy or Kaz broker one can buy them i believe. However many retail brokers will struggle to help a client sell.

also in normal shares territory:

Coface, Spirit Airlines, Whitehaven coal, Triple Flag Precious, EML Payments and Diversified Energy.

Interesting you mentioned coface – its already been looked at, might do. Whitehaven coal – I own some already, but not much. Will check out the others thanks..

I forgot to mention Vonovia, a pretty large holding of mine .. based on some guess of mine that rate reductions will help it and the German property sector, its also got ultra low financing in place so has in my view been beaten down rather too much. Though its already gained a fair amount since i bought.

RBI ( Raiffeisen Bank) has also been a great stock for this year, but its a small holding of mine

I also looked at RBI – but was too slow. Thanks

Noticed you are looking at tobacco – on the Danish exchange there is Scandanivian Tobacco (STY) who are the primary way of investing Cigars and Pipe Tobacco.To trade them though i think you would have to open an account with Saxo bank.

Had a look at them but debt is too heavy for my liking – will check out Scandanavian tobacco.

Thanks for the comments and update.

Personally I was up 14.9% this year which is very disappointing given that I was 80% invested in uranium equities and 5% $YCA (in and out).

Hard to understand actually as 3 of the 4 biggest holdings which make up 50% were up between 40% and 55% with the other one down 17%. Maybe a mistake on my spreadsheet. The move in the dollar hasn’t helped.

I know I’m down about 20% since the uranium sector highs back in April 22. In that rally my stock picks outperformed $URNM and $YCA but not so in the latest rally to date which has favoured the larger market cap. equities.

I’m going to put about 5% in a physical gold ETF next week. I may also move a decent percentage out of my uranium equities into $YCA for a safer approach but I do feel my holdings should catch up if there’s no general fall in equities.

I hold about 5% in $GKP after seeing your comments and following the story. I did hold $AZZ, $THS, $SQZ and $JEMA but sold them to buy $YCA and $GKP.

I also maintain a value of 0.35% of portfolio value of 1 year out put options with a 25% discount strike price to the current index prices on the S&P 500 and QQQ. I have doubts whether these will provide the hedge I need in case of a 20% downturn in those indexes but I read something on options that you tweeted about and it mentioned some guy making 60X on equivalent put options back in 2007/8. My own experience with options as a hedge historically has been that they’re too expensive but I’ve always gone for shorter dated ones.

Best of luck for 2024.

Cheers John – irritating you seem to be doing better than me with many of my ideas! $HAUTO might be worth a look for you – have a look at their presentation…